Liquidity in the Time of Cholera

Prediction Markets in Public Health

The world was undone the last time a pandemic hit. A civilization that can price ten years of cash flows in a millisecond could not price, in time, the catastrophe under (and in) our noses.

Certainly, every piece of evidence we needed to predict COVID was available: a cluster of sick employees was noticed by an employer in China, an overrun waiting room by a charge nurse in Brazil, a supply chain tightening by a commodities trader in New York. Still, by the time it hit the press and political pundits, the pandemic was unstoppable. And what could we even do about it?

Erring on the side of caution is not ideal. Nobody has ever been promoted for buying ventilators a month too early. Nor does anybody want to explain a school closure that was unnecessary.

And although the CDC serves a much needed role, as a centralized agency, it is inherently slow. There is a long pipeline that information must travel: first, labs go from hospitals to regional/university centers who run the initial testing. This data is then pushed out to state epidemiology agencies who run their own risk models and do further testing. Finally, many days later, this information is forwarded to the CDC, who usually waits until Thursday, around 1 PM ET, to publish the official MMWR report.

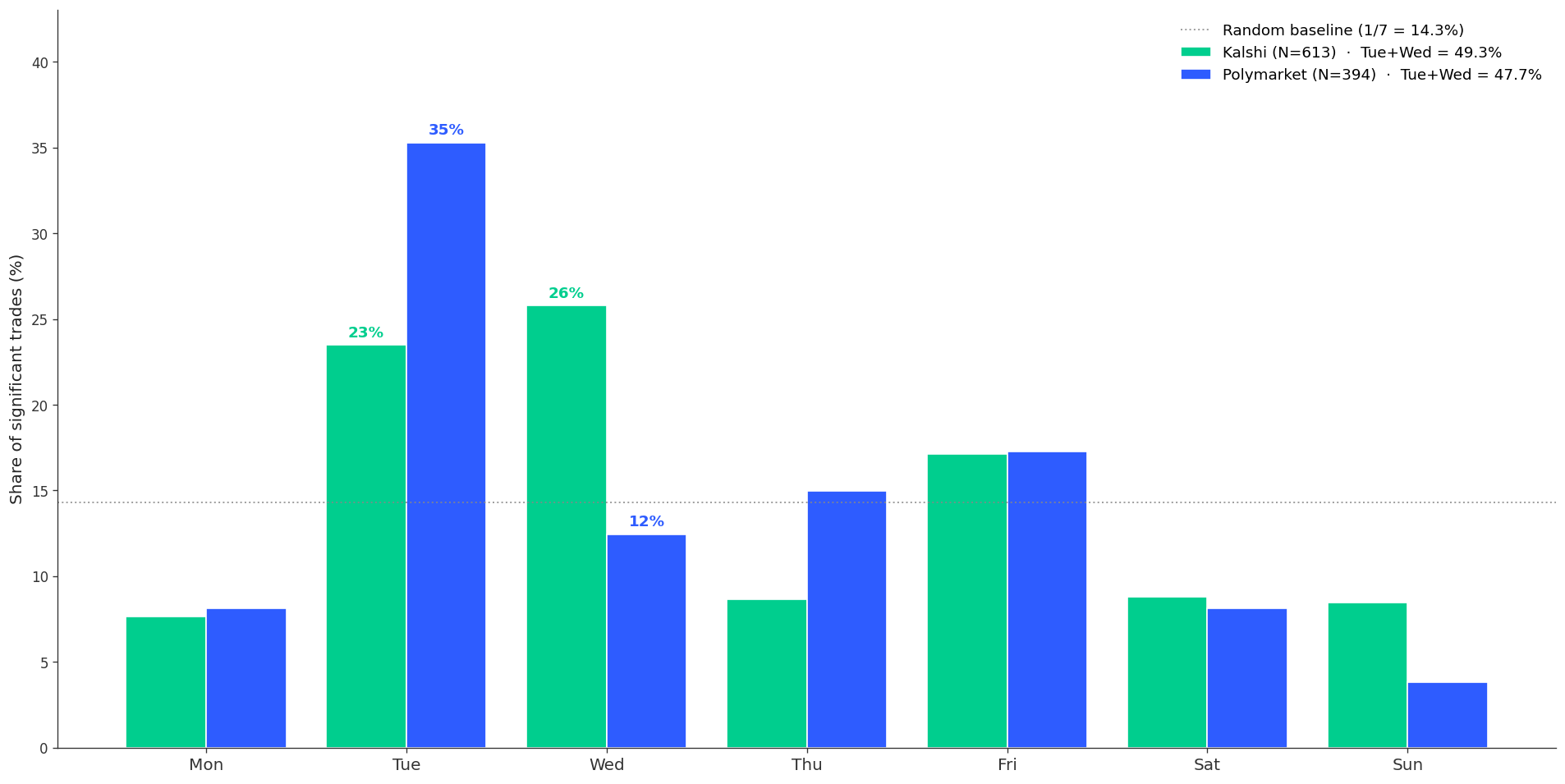

I have been closely following the spread of measles and was curious whether anybody within this aforementioned chain had been front-running the Thursday CDC reports on Kalshi or Polymarket. I found that, on the Kalshi market, “Measles cases this year?” 49.3% of significant contracts (>$300) were traded on the two days leading up to the CDC report being released. I also pulled the trades from the analogous Polymarket event and across 71,071 fills, Polymarket’s yearly market has 47.7% of >$1,000 trades on Tuesday and Wednesday.

It is possible that this imbalance stills from state data getting released early. But, generally, the dashboards from states update uniformly randomly throughout the week, and so we would see a much more uniform graph if that was the case.

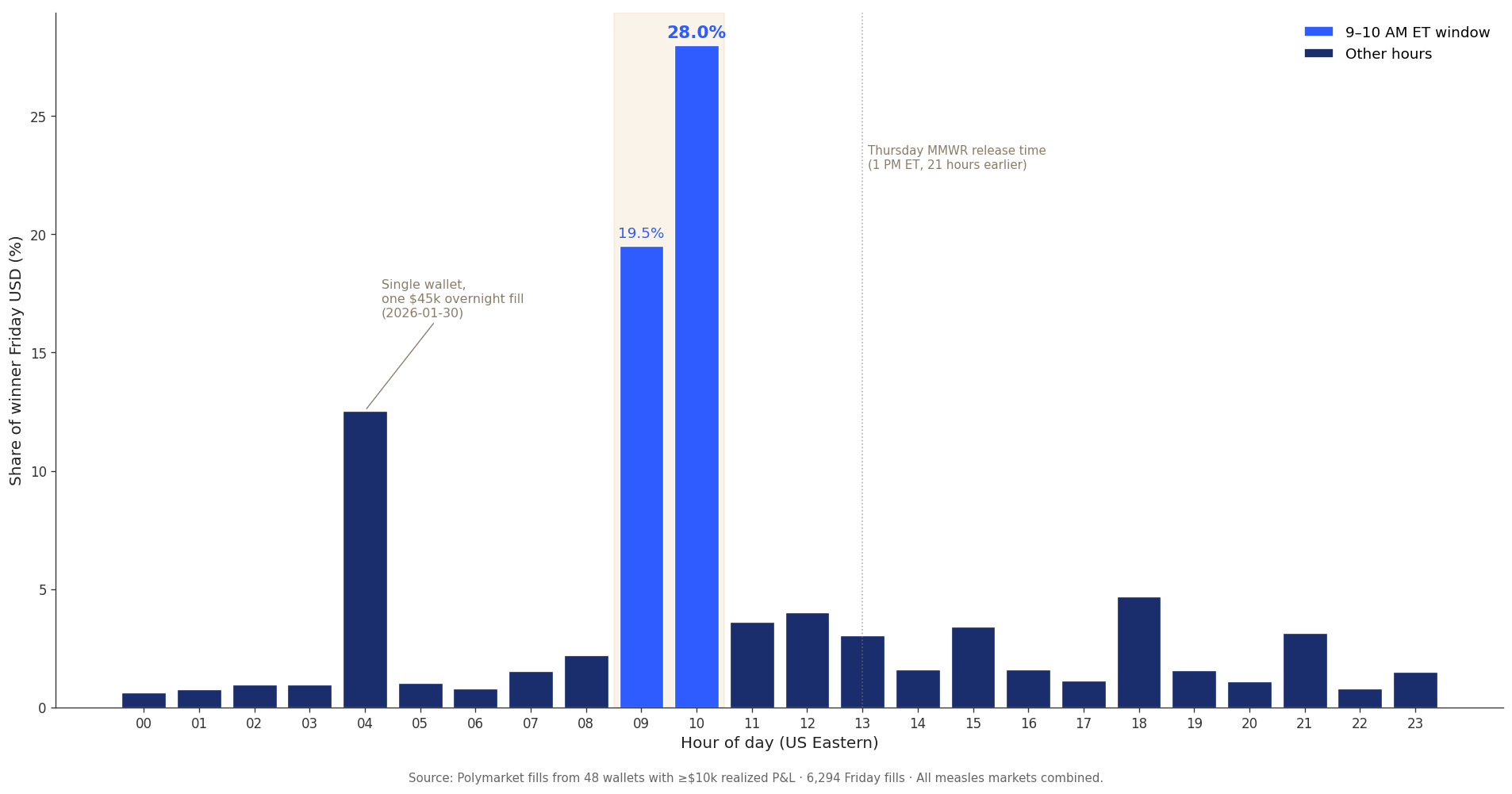

The Polymarket data has more granular monthly markets for measles too, which surprisingly do not have this pattern at all. For some reason, the distribution is flipped, with whale activity concentrating on late Thursday and Friday. The wallets that consistently make money on measles trade on Friday between 9 and 11 AM Eastern, often right at 10:00. Across fourteen Fridays in the dataset of monthly measles markets, ten had their peaks in that two-hour window, the sharpest on March 20, putting nearly 90% of its volume into it. It is probably safe to assume this is coming from traders buying the post-MMWR mean reversion once the news cycle has processed overnight and many square traders have taken positions.

It is not terrible even if there are potential insiders on these markets. The Polymarket measles market will never be able to replace an organization like the CDC. But it remains an incredible convenience to society to be able to aggregate insider opinion in a way that sidesteps formal channels and allows the public to view forecasts of the disease as quickly as possible and, on Polymarket specifically, to do so with trades that are timestamped, wallet-addressed, and visible on-chain to anyone curious enough to look.

One line that still seems vague is determining at what point disease markets become bioterrorism markets. CFTC 40.11 specifically prohibits contracts that involve terrorism and assassinations. And certainly if Kalshi can argue that the “Khamenei out” market a death market and halt it, then a similar argument can be made to show measles markets are bioterrorism markets. These markets are relatively illiquid and the lines on # of infections are wide, so it is not worth it for someone to superspread. In a future where a prediction market on a rare disease could get opened and gain a significant amount of liquidity, we should be terrified.